ASB Financing (ASBF) is one of the most talked-about wealth-building strategies among Malaysians — but many people don’t fully understand how it works, what the risks are, and whether it actually makes financial sense. This guide breaks it all down for you.

- ASBF lets you borrow money from a bank to invest in ASB — amplifying your returns through leverage

- Only Bumiputera Malaysians are eligible to invest in ASB and apply for ASBF

- ASBF works best when ASB dividend rate exceeds your loan interest rate

- You still need to pay monthly instalments regardless of ASB performance

1. What is ASB and ASBF?

Before diving into ASBF, let’s understand ASB first. Amanah Saham Bumiputera (ASB) is a unit trust fund managed by Amanah Saham Nasional Berhad (ASNB), a subsidiary of PNB (Permodalan Nasional Berhad). It is exclusively available to Bumiputera Malaysians and has historically delivered consistent dividends year after year. You can view the official ASB fund details on the ASNB official website.

ASB Financing (ASBF) is a loan product offered by Malaysian banks that allows you to borrow a lump sum to invest in ASB. Instead of saving up RM100,000 over 10 years, you borrow it now, invest it immediately, and use the ASB dividends plus your own monthly payments to repay the loan. The idea is that your money works harder from day one.

💡 MyFinanceMemo tip: ASB is not the same as ASB2 (Amanah Saham Bumiputera 2). Both are available to Bumiputera but have different unit structures and dividend histories. Most ASBF products are for ASB (fixed price at RM1 per unit).

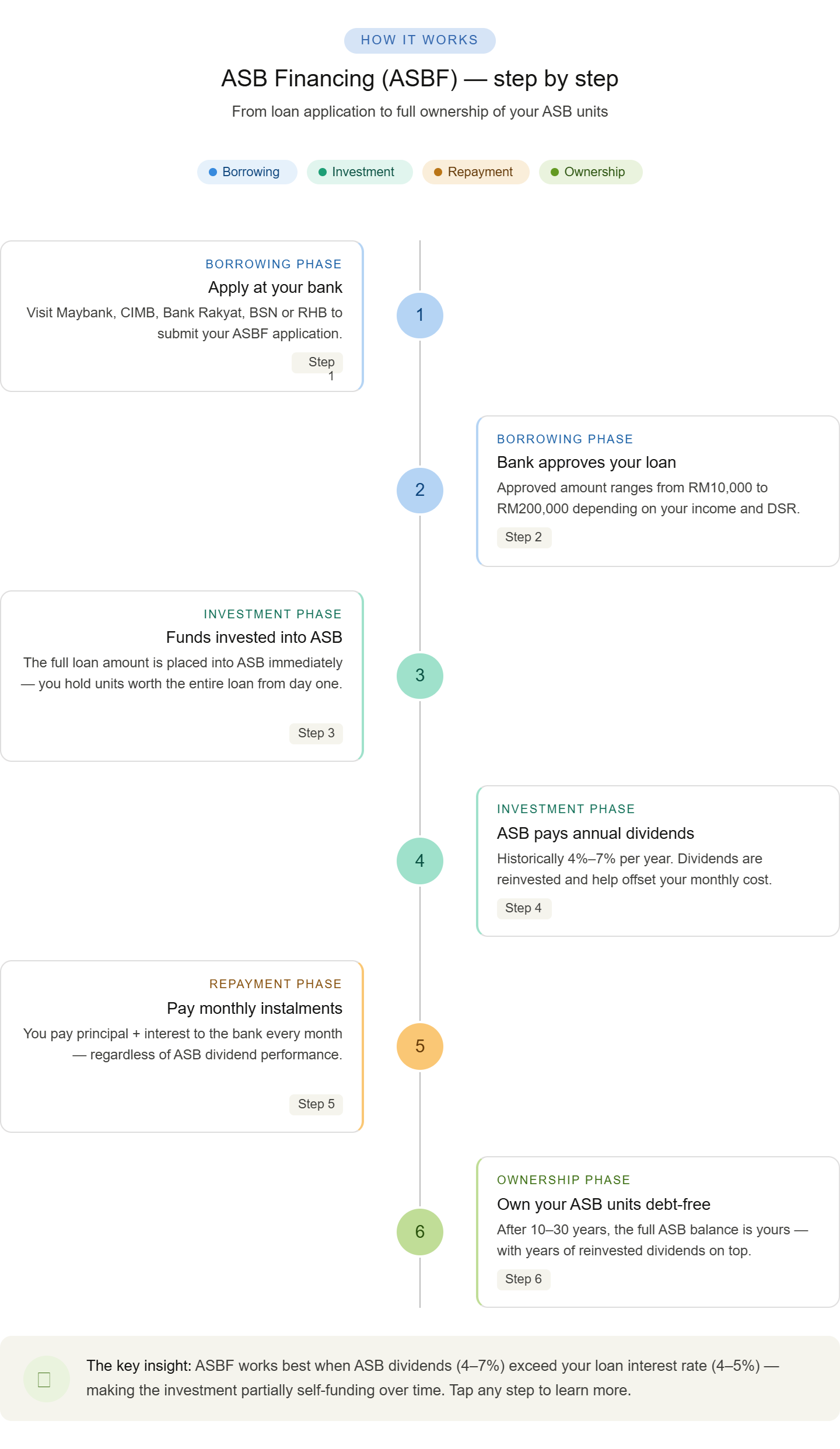

2. How Does ASBF Actually Work?

Here is a simple step-by-step of how ASBF works in practice:

- You apply for ASBF at a bank — Maybank, CIMB, Bank Rakyat, BSN, or RHB are the most common providers.

- The bank approves a loan — typically between RM10,000 to RM200,000 depending on your income and eligibility.

- The loan amount is invested directly into ASB on your behalf — you now have ASB units worth the full loan amount.

- ASB pays you annual dividends — historically between 4% to 7% per year on your total units.

- You pay monthly instalments to the bank — covering the loan principal plus interest.

- At the end of the loan tenure (typically 10–30 years), the ASB units are fully yours with zero debt.

3. Real Example — Does ASBF Make Money?

Let’s use a real-life example to see if ASBF makes financial sense:

Scenario: Ahmad takes an ASBF loan of RM100,000 for 30 years at an interest rate of 4.5% per year. ASB pays an average dividend of 5.5% per year.

| Item | Amount |

|---|---|

| Loan Amount | RM 100,000 |

| Monthly Instalment | ≈ RM 507/month |

| Annual ASB Dividend (Year 1) | + RM 5,500 |

| Annual Loan Interest (Year 1) | – RM 4,500 |

| Net Gain (Year 1) | + RM 1,000 |

| Total Interest Paid (30 yrs) | ≈ RM 82,000 |

In this scenario, Ahmad’s ASB dividend income exceeds the loan interest — meaning the investment is effectively partially self-funding. After 30 years, he owns RM100,000 worth of ASB units (plus accumulated dividends reinvested) while having paid roughly RM82,000 in interest. Whether this is “worth it” depends on what he would have done with the RM507/month otherwise.

4. Who Should Consider ASBF?

ASBF is not for everyone. Here’s a simple guide on who it suits best:

- ✅ Good for: Bumiputera with stable income, long investment horizon (10–30 years), and discipline to pay monthly instalments without fail.

- ✅ Good for: Those who want to build a large ASB position quickly instead of saving slowly over decades.

- ❌ Not ideal for: Anyone with unstable income, existing high debts, or who may need the money soon.

- ❌ Not ideal for: Those who cannot comfortably afford the monthly instalment on top of existing commitments.

💡 MyFinanceMemo tip: A good rule of thumb — your total monthly debt commitments (including ASBF) should not exceed 60% of your monthly income. Use our loan calculator to check your instalment amount first! You can also check your credit standing anytime via BNM eCCRIS.

5. Which Banks Offer ASBF and What Are the Rates?

Most major Malaysian banks offer ASBF. Here’s a comparison of common providers:

Always compare the Effective Interest Rate (EIR) — not just the advertised rate — when choosing a bank for ASBF. Bank Rakyat is often favoured for its fixed rate structure which protects you from OPR changes. You can track the latest Bank Negara Malaysia OPR history to understand how floating rates are affected.

6. The Risks of ASBF You Must Know

ASBF is not without risk. Here are the key risks to understand before signing anything:

- ASB dividend is not guaranteed — While ASB has consistently paid dividends, PNB is not legally obligated to maintain any specific rate. You can check the ASNB official site for the latest declared rates. If dividends drop below your loan interest rate, you pay more than you earn.

- You still owe the bank regardless — Even if ASB pays 0% dividend in a bad year, your monthly instalment is still due. Missing payments affects your CCRIS/CTOS credit record. Check your credit report anytime at BNM eCCRIS.

- Opportunity cost — The money paid in instalments could have been invested elsewhere, potentially at higher returns.

- Long commitment — A 30-year loan is a serious commitment. Life circumstances change — job loss, health issues, or family needs could make repayment difficult.

“ASBF is a powerful tool when used wisely — but it is leverage, and leverage amplifies both gains and risks. Never borrow more than you can comfortably repay.”

— MyFinanceMemo Editorial Team

- → ASNB Official Website — ASB fund info, dividend history & investor portal

- → PNB Official Website — Parent company of ASNB

- → Bank Negara Malaysia — OPR & Monetary Policy — Track interest rate changes

- → BNM eCCRIS — Check your personal credit record before applying

ASBF is a legitimate and popular wealth-building strategy for eligible Malaysians — but it works best when you go in with clear eyes. Make sure the monthly instalment is comfortable, the loan tenure fits your life plan, and you understand that dividends are not guaranteed. If in doubt, start small — a RM50,000 ASBF is a great way to experience the strategy before committing to a larger amount. As always, consult a licensed financial advisor before making any borrowing decision. Found this helpful? Share it with your family and friends who are considering ASBF!

⚠️ Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. ASBF involves borrowing and investment risk. Please consult a licensed financial planner before making any financing or investment decisions.